Archives

Contractors: Adopting Enterprise Risk Management or Falling Behind?

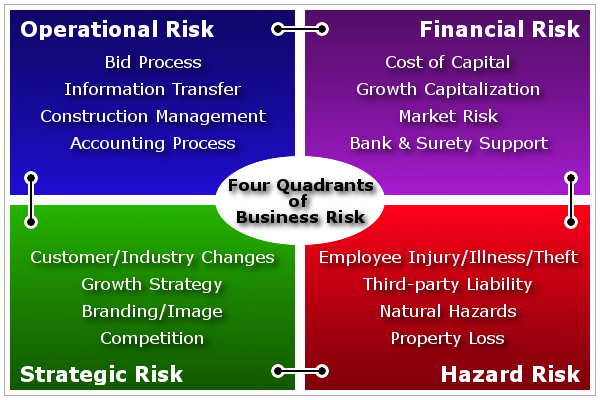

In this post, we’ll give some background on the growth of Enterprise Risk Management and how it relates to the construction industry, and explain why adopting an Enterprise Risk Management philosophy for running your construction business is a wise decision. We say philosophy, because at its core, ERM is a shift in thinking, a shift in managing your business. It applies best in high risk industries, like construction, which have high failure rates due to persistent failures to recognize and mitigate risk across the entire business. Enterprise Risk Management Growth In a 2001 survey, Enterprise Risk Management: Implementing New Solutions, it was noted that 41% of the public companies surveyed indicated that they were currently implementing some form of ERM program. As a result of Sarbanes-Oxley Act (aka SOX, the compliance requirements set forth after the Enron debacle), that number has been climbing ever since. Why? Quite simply, the rules of the game have changed for public companies. They must now prove they have strong internal controls, complete intregrity and systems to manage all risks they face. Unexpected “surprises” are no longer accepted; they now have swift consequences. Given this environment it’s no wonder that Enterprise Risk Management (ERM) is being adopted by public companies at an ever increasing pace. In the United States, the Securities and Exchange Commission, as well as the U.S. Federal Reserve and the American Institute of Certified Public Accountants, are demanding more accountability from corporate directors in terms of identifying risks and developing systems for managing them. The National Association of Corporate Directors is encouraging audit committees to expand their scope of risk management reviews. Dunn and Bradstreet has released software to provide ERM Solutions. Standard & Poors, one of the largest credit rating companies of businesses worldwide, has announced that it is now including questioning about a company’s ERM practices to determine ratings for credit. This rise in expectations requires a level of risk management knowledge and capability not found in many organizations, so companies are scrambling and reacting to institute risk-based controls. But how does all this apply to private companies that don’t have to worry about compliance issues brought forth by SOX? Plainly stated, ERM is not just for the “Big Guys” anymore. As Tim Ling, president and chief operating officer of Unocal, stated: “I think you will see almost all companies over the next few years moving in the same direction [as we are], really trying to integrate the notion of risk management with the notion of just business management. To me, running a business is all about managing risk.” Essentially, managing risk is really about properly managing a business, and therefore managing risk can create shareholder value if done correctly. Thus, ERM is now seen less as a reactionary requirement to regulations, and more as just plain old good business practice. In fact, according to the RIMS 2011 ERM Benchmark Survey, over 75% of the 14K public and private companies in the survey had active ERM programs or were investigating ERM adoption: Why Contractors make good Candidates for ERM Does ERM apply to contractors? Yes, more than ever. Since ERM best fits companies in high risk fast moving industries, contractors are prime candidates for adoption. Here are some reasons why: All of these characteristics make contractors great candidates for ERM. So let’s talk about the how ERM can actually overcome the challenges for implementing risk controls as stated above, namely: the abundance of construction risk, the time constraints upon management, the insufficient knowledge about ERM and unstable controls. How ERM overcomes the challenges for implementation of risk controls Takeaways In short, ERM addresses an abundance of risk by following a systematic process that educates the workforce on elements of risk within their area of responsibility, empowers them to individually install risk controls which are then monitored within the process to make sure the controls remain fully in place, thus creating a “no surprises” management environment. Without an ERM framework, the failure to recognize risks or to mitigate known risks can make it difficult to compete, financially weaken the company, and potentially jeopardize its future. So there you have it. ERM is being adopted worldwide and it is a perfect fit for construction. It will just be a matter of time before you will be expected to run your business with a risk-based approach. In fact, banks and sureties are already asking contractors, “Who handles enterprise risk management for your company?” Do you want to be the company that lags behind in understanding and taking action on business risks, or do you want to be a survivor in today’s fiercely changing and competitive environment? As to the ultimate question: “Should I personally get engaged in a risk-based mindset and adoption of ERM,” we leave you with some final questions: To learn more, contact Druml Group for construction enterprise risk management solutions.Construction Insurance: Tips for Purchasing Contractor’s Insurance

Purchasing insurance is a dreadful task. Not only is it money out of pocket, but many brokers and insurance carriers seem to talk in a foreign language. In this post, we discuss three tips to help combat the confusion and ease those insurance pains. After reading, you will be ready to speak the language and understand insurance terms. This will keep you confident at the negotiating table. In addition, the pointers will save you money and reduce unexpected financial shocks. 1. Negotiate with the RATE, not PREMIUM Contractors are very busy and like to get right to the point. “What’s it going to cost me?” Cost translates directly into premium. However, the smarter question would be, “What is my rate?” RATE Definition The dollar amount paid for each $1,000 of REVENUE or $100 of PAYROLL. Example With a RATE of $11.5, ABC Contractor Inc. will pay $11.50 in premium for every $1,000 of revenue. EXPOSURE Definition The total REVENUE or PAYROLL whose corresponding liability will be covered by the insurance carrier. Example ABC Contractor Inc. estimates revenue at $9.5 million. PREMIUM Definition Total cost of an insurance policy (excluding broker or policy fees). Example ABC Contractor’s general liability is provided by USA Insurance Inc. for a PREMIUM of $109,250. The RATE multiplied by the EXPOSURE equals the PREMIUM: ($11.50/$1,000) X $9,500,000 = $109,250. Since EXPOSURE can fluctuate from year-to-year, PREMIUM alone is a poor metric of comparison. For instance, there’s a big difference between paying $100,000 for $5 MM of sales than for $20 MM of sales. Using the RATE, instead of the PREMIUM, will ensure your year-to-year comparisons are accurate, regardless of revenue growth, stagnation, or reduction. Negotiating with the RATE places the contractor in a better position. For example, ABC Contractor Inc. performs 10% more work than last year. The insurance carrier explains that the 10% PREMIUM increase is entirely due to the increased business. That makes sense. However, contractors strive for continued savings. A larger EXPOSURE usually means your can negotiate a lower RATE. Ignore the PREMIUM when negotiating insurance and focus on lowering the RATE. 2. Compare the RATE Year-to-Year Be careful. Although the RATE is a better number for comparison from year-to-year, it can also be affected by LIMITS, COVERAGE, CLASS, and LOSS HISTORY. LIMITS Definition The most a carrier will pay for claims against the policy. Example ABC Contractor Inc’s auto policy will cover liability up to $1,000,000 per accident COVERAGE Definition The types of losses that trigger an insurance policy to pay. Example ABC Contractor Inc’s general liability policy covers bodily injury or property damage to a 3rd party. CLASS Definition The risk associated with the type of work the contractor performs. Example The insurance rates for Riley’s Roofing are high because roofing is a dangerous CLASS of work. LOSS HISTORY Definition The history of claims made against a company; usually over the last 3 to 7 years. Example ABC Contractor Inc’s new insurance carrier requested a loss history to see if there were any previous losses that would indicate ABC Contractor, Inc. was risky client. All these variables play a role in determining a RATE. If none of those variables have changed from year-to-year, then the goal is for the RATE to be lower or at worst the same. Changing the LIMITS and COVERAGE are easy to do. Sometimes changes are necessary to meet the requirements of one unique project. The more changes that are made, the less RATES can be compared between years. Lowering LIMITS and COVERAGE may leave a company exposed. In our Construction Business Viability Analysis, one of the risk factors examined is “Ignoring Insurance Needs.” When money is tight, contractors often fall into the trap of reducing or canceling coverage altogether. Every reduction can cause a gap. The small savings today may result in a large expense down the road. LIMITS and COVERAGE should be analyzed on a needs basis and not a price basis. 3. Be Prepared for the Final Audit At the end of the policy period, most liability policies will have a final audit to adjust the estimated EXPOSURE with the actual EXPOSURE. AUDIT PREMIUM Definition PREMIUM due as a result of differences in the estimated and actual EXPOSURES. Example ABC Contractor Inc. actually made $10.5 million in revenue, $1 million more than originally estimated. The extra $1 million at the same 11.5 RATE produces an AUDIT PREMIUM of $11,500. MINIMUM EARNED PREMIUM Definition The lowest amount of PREMIUM an insurance carrier will retain. Example ABC Contractor Inc. had a horrible year with revenues of only $6 million. Since the insurance policy had an 80% MINIMUM EARNED PREMIUM based on an EXPOSURE of $9.5 million, ABC Contractor Inc. will still be charged for an EXPOSURE of $7.6 million (80% of $9.5 million). Final audits can cause a great deal of heartache. If a contractor hasn’t been properly accruing insurance expense, what was a good year could turn sour when the AUDIT PREMIUM hits. Inaccurate insurance accrual is identified by the risk factor “Inaccurate Accounting.” AUDIT PREMIUM shouldn’t be a slap in the face. During the entire year, the accounting manager can determine the expected price of the AUDIT PREMIUM by comparing overall revenue to the estimated EXPOSURE. This was the subject of a recent Case ‘n Point article. In reverse, the MINIMUM EARNED PREMIUM is designed to catch overestimating. Contractors may try to reduce the RATE by increasing their EXPOSURE (i.e. estimate $25 million, lock in a low RATE, then end the year with only $15 million in sales). However, insurance carriers have placed MINIMUM EARNED PREMIUM conditions in the insuring agreement to avoid this type of gaming. Avoid making optimistic estimates as the consequence will hit harder than the savings. Final Thoughts Insurance renews once a year. Since you can’t be an expert, brush up on the details when your renewal comes around so you can speak to your broker with confidence, and ensure they are getting you the best deal possible. In summary, we’ve provided... Read MoreIn Construction, Cash is King

A few days ago I met a fellow after doing laps in the pool, ala Michael Phelps! (I’d like to think we know as much about construction as Michael knows about swimming.) We began talking and sure enough he was the proud owner of a thriving construction company… but it wasn’t always that way. In fact, he shared with me the trials and tribulations he had experienced in the construction business. We laughed about the scrutiny his work received when doing custom mansions for the very wealthy. And then we talked more seriously about a dramatic change in his career. You see, this strong willed Irishman was a victim of a key risk factor: Mismanagement of cash flow. He shared with me how cash flow had put him out of the construction business. His claim to fame was the installation of high end custom wood work in plush offices and homes. As he became bigger, he just was not prepared for the cash flow crunch that he would experience. He shared with me his frustrations at getting paid from General Contractors who always had an excuse for not paying, and he used a few choice words. It was obvious that he had experienced what has put so many companies out of business, a cash shortage. He indicated he was making good money, and I believe that because custom millwork brings a good margin and there is not a lot of competition for highly specialized woodwork. He had different types of wood shipped in from all over the world and he shared with me how even though he was profitable, when he pursued the bigger work, cash flow became too much of an issue and he was forced to reinvent himself. This certainly is a familiar story.Construction Failure: Why Contractors Fail

The construction industry is full of unending challenges, requiring high energy and constant problem solving. The company owner is like a juggler with 50 balls up in the air (potential problems); if any drop (actual problem) it could cause all the rest to drop as well (total problem i.e. business failure). The large amount of potential problems, combined with low industry margins, is undoubtedly a major reason the construction industry has one of the highest failure rates (right up there with restaurants). Unlike companies in most industries, though, contractors usually don’t fail because of poor products or service. Why Contractors Fail Sure there are some cases, but in general, contractors don’t fail because of poor construction. Most contractors build a decent building. After all, they have to follow rigid design specifications and plans and have to undergo inspections. So if they don’t fail because of poor building practices, then why do contractors fail? In simple terms, it is because of poor business practices. Many construction companies are started by project managers without specific schooling in running a business. They know how to run a job, but haven’t been taught to run a construction company. To compound matters, there isn’t really much formal education offered in running a construction company. Frankly, there should be a college major for it. Finding the Root Causes of Failure Every company has a bunch of business practices, and if those business practices are properly in place, the company will maximize its ability to make a profit. All those business practices (or things you need in place) are called risk factors. That is the heart of Enterprise Risk Management: Every process, practice, system, procedure, or activity that takes place in a company must be working perfectly to maximize profitability. Obviously, this sort of perfection is impossible, but it is (or should be) a goal for every company. So, we started on a quest to uncover the root causes of business failure. We began by identifying all of the major contributing causes for loss based upon our years of experience and sought out publications and other professionals who could serve as resources for further adding to the list. We knew that all causes of loss could be fixed by putting a business practice or control in place and that if those controls or practices weren’t in place, it could cause a business to fail. Conversely, having all the necessary controls and practices in place would provide a business with the greatest ability to generate profits (to maximize profitability). With a greater understanding of how controls impacted profitability, it became clear that the effectiveness of existing controls at a company had to be assessed to determine the degree the company was at risk of failure. This is, in fact, what the Enterprise Risk Management process does and what risk management was intended to be long ago. Reactive Management Just like financial advice is sought after a portfolio has shrunk or a financial dilemma has occurred, and business analysts are brought in after a company has lost money, we spent our early days as consultants patching up systems or procedures in construction firms that were disheveled. In fact, a large amount of our time was spent on complete turn-arounds. It made us feel like lawyers, always looking in the past at what went wrong rather than looking toward the future and preventing problems from occurring. That really isn’t the best business philosophy… that is, to bring in an expert after something is messed up. A much better business philosophy is one that prevents “mess-ups” from occurring in the first place, which is why Enterprise Risk Management is so well suited to construction. Proactive Management Enterprise Risk Management identifies potential causes for loss well in advance so they can be addressed before harm occurs. This is a large shift from the thinking of fixing problems once they occur. That is the beauty of ERM. It prevents problems by recognizing weaknesses while they can still be corrected. That said, most contractors continue to unknowingly risk profits by failing to inspect systems and controls that could cause future problems. Let’s get back to our project manager turned business owner. Without the proper educational tools or experience actually running a company, his chances of survival are low, which is exactly what the statistics show. To increase his odds, he should study the business practices (risk factors) necessary to run a construction company effectively; there are at least 79 which are important to a company’s success. We encourage any contractor interested in preventing problems rather than patching them to consider adopting an ERM process and the philosophy of enterprise-wide risk management. It’s a sure way to strengthen business fundamentals and maximize potential profit.